Free write-up | TMT Series #4: Toast, empowering the restaurant ecosystem through technology

Is Toast toast or can it still become the bread? A look at a leading operating system for the restaurant industry

Toast is a restaurant payment processor company which sells software and hardware to help restaurants conduct sales, manage orders, and plan a marketing strategy. Its S-1 claims that the company is “democratizing technology” which can help restaurants of all sizes compete on an even playing field.

Since its IPO in September, share price performance has disappointed in light of macro headwinds and modest levels of profitability bringing share price to all time low of $24.2 per share as of January 18th, the question remains, can these levels represent great entry points?

In this latest issue of Golden Lake’s Tech Series, I go over Toast’s products and business model, its main competitive advantages and determine to what extent can catalysts help bring the stock up and allow the retail investor to make good profit in a long time horizon. Enjoy!

Overview

Product:

(click to enlarge)

Toast offers a cloud-based system to quick serve (QSRs) and full service restaurants (FSRs), with a modular all-in-one restaurant management platform encompassing POS, payments, operations management, online ordering, self-serve kiosk ordering and checkout, inventory management, loyalty program management, gifting and myriad of other restaurant needs. Toast’s Android tablet-based cloud solution is beating out other new systems head to head and more impressively attacking on prem proprietary hardware incumbents Micros and NCR, who together make up 50% of the market.

While there are a handful of “next gen” players attacking this market, Toast has a significant early advantage. First off, the sheer amount of software the team has built in a short span is impressive – feature for feature they are already much more in the class of the >20 year old enterprise systems than the next gen “Bistro” players, and so for restaurants with any level of sophisticated feature requirements they win easily. But beyond just being very good at building good product quickly, the company also made two smart choices that sets them apart from the other players.

First, while competitors have almost all built on iPads/iOS, Toast’s Android-based architecture allows restaurants to be much more flexible in their hardware choices (iPads are simply not enterprise grade and come in far fewer form factors than Android), has fewer software versioning issues than iOS and the upfront hardware costs are cheaper.

Second, Toast also did real work to build out transaction processing capability, which lets them subsidize their fees by operating as a transaction processor (they simply match current restaurant rates and almost always win the transaction business without objection.) This allows Toast to price competitively and earn a much higher margin than competitors head-to-head.

However, Toast’s product is still very immature, and every day they roll out new features like online ordering and inventory management. Despite that, I believe Toast is a leader in its category, this assessement is backed-up by the fact that:

Toast beats every major competitor head-to-head in sales scenarios by a significant margin (other than for a feature that they have not built yet). Combing through all of their loss explanations that I gathered through expert interviews, it seems that they only lose based on either an owner who has already selected another system, or on price, and there just at the low-end of the market

Toast churn is driven almost entirely by restaurants going out of business, and they have never lost a customer to another cloud-based POS, whereas they have stolen several customers from their competitors. Occasionally they will lose a customer in a complex location where wifi issues make handheld tablets (part of the Toast value prop for some buyers) difficult and in those cases the owners tend to revert to legacy systems but remain big fans of the Toast product.

Toast net retention and upsell across multi-unit locations has been a big growth driver – many times a one unit pilot has turned into a multi-unit adoption

Key Purchasing Criteria:

Beyond combing through their salesforce data, I have spoken to several Toast customers – in addition to the 12 references provided by the company and the feedback has been overwhelmingly positive, producing an informal NPS of over 80 with only one mild detractor. Encouragingly, customers favorite Toast features yield a large range of answers:

It’s intuitive and really easy to use:

Much more efficient than legacy systems on key workflow activities. Occasionally an owner will mention something that could be improved and are always amazed when the software improves the next week…

Really easy for a new employee which means reduced time training

Cloud solution – multiple users cited benefits of the cloud including:

Make updates or review analytics from anywhere. An owner can set alerts giving them visibility throughout the day on performance at any location, or in a particular server area

Feature improvements – impressed at the rapid deployment of new features to make the product even better

No more server crashes. If anything stalls it’s only just for a minute and the devices can operate in offline mode so no outages

Integration with third party software – several users favor another third-party restaurant solution (like a loyalty program or inventory tool) and Toast has been able to easily integrate into these solutions.

Table-side hardware drives throughput efficiency:

Allows servers to send orders immediately to the kitchen

Guests can run credit cards at the table – and give dynamic feedback on service

Many customers have seen significant increase in table turns and service speed

CRM:

Guests receive receipts by email (this also speeds up line throughput in QSRs/cafes), and restaurant has entire order history easily accessible which allows for analysis on best guests, quick retrieval of a past receipt, etc.

Other advanced features such as online ordering, website menu integration, integration with other third-party software, etc.

Bottom line: Toast is a stand-out product which is driving the company’s early success, and there is a ton of potential for the product to improve with modules for mobile checkout, scheduling, inventory management, CRM, and others just getting started.

Go-to-market/sales strategy:

Toast is primarily selling direct to SMBs today via an inside sales force, but the company is also in the early stages of building out a channel strategy. The company claims that the Micros acquisition has been painful for their VAR channel and is freeing up many VARs in search of new solutions to sell. Toast’s most notable channel partner to date is Gordon Food Service, a distributor to >100K locations who are pushing Toast and an integration to their food costing/ordering service – GFS accounted for about 25% of Toast bookings this year.

The sales effort to date has been effective, but I believe highly under-optimized. Both SMB and enterprise sales are being run by co-founder Aman Narang, an ex-star product leader at Endeca who had previously never sold anything in his life. Room for improvement is also clearly evident on the marketing side; a search for “best restaurant POS” will show Toast only several pages deep.

Most exciting is Toast’s ability to push into the mid-market chains which have much more volume per location and thus monetize at a much higher rate, and have sophisticated needs that drop away all of the competitive noise as no cloud POS other than Revel (which I think is an inferior product with a bit of a head start) can compete at this level.

Marketing for Toast has been largely organic with trade shows driving some leads, but many leads coming in from restaurants researching solutions or hearing about or seeing Toast out in the market.

Team:

I believe this is the best product team in the POS space. CEO Chris Comparato and co-founders Steve Fredette, Aman Narang, and Jon Grimm were A players at Endeca, and the team is extremely hungry working all hours obsessed with building out the best product the restaurant industry has ever seen.

Chris Comparato, CEO: Chris joined Toast in 2015 from Acquia, where he was SVP of Customer Success. Prior to Acquia Chris was SVP Worldwide Solutions at Endeca and was Steve Papa’s best operator. I have been impressed so far with Chris although this is his first full CEO role.

Steve Fredette, Co-Founder: Steve is a world-class product/engineering unicorn, and previously led pre-sales and product at Endeca. He focuses more on product and engineering at Toast.

Aman Narang, Co-Founder: Aman currently helps run Product as well as Toast’s inside and field sales efforts, and has performed impressively in the role given a background otherwise totally devoid of sales experience. Previously, Aman was a member of the product leadership team at Endeca. I’m not sure where Aman’s focus will settle in the long run, but he’s extremely talented and has a ton of upside potential.

Jon Grimm, Co-Founder: Jon is currently focused on technology—making sure the product works at all times including payments. Tech is a massive challenge here as restaurant customers don’t tolerate a minute of product downtime and Jon has performed admirably although has a big challenge on his hands to keep the tech performing as the company scales.

Market landscape:

There are approximately 1 million addressable restaurants in the US, and with current ARR / location around $5,000 and upside with additional product features potentially approaching $10,000, I estimate the market size at $5 – 10 billion. This is large, but maybe not surprising relative to the $600B Americans spend at restaurants every year.

Approximately seven in ten of these million restaurants are “independent” often single location operations, as opposed to chain stores, although a significant fraction of these “independents” have shared ownership or multiple locations. Toast’s core demographic today is independent operators but they have begun to move into “mid-market” 10-200 location chains as well.

The likely sweet spot for Toast is the combination of larger independent restaurants and “mid-market” chains – approximately 300-400K of the 1M restaurants fall into this sweet spot. Over time I think any restaurant that uses meaningful software should be a Toast customer.

Competition:

In addition to being massive, the POS market is extremely fragmented, with two large incumbents, Micros and NCR, each accounting for roughly 25% market share. Beyond these two big players there is a growing list of cloud challengers, including:

Revel: Early leader in the iOS tablet market and has raised >$100MM. iPad based.

Breadcrumb: Feature-light POS acquired by Groupon.

POS Lavu: iOS.

Clover: extensive distribution, low upfront cost and proprietary hardware.

Square: For basic single countertop and cash register restaurants only - no true restaurant operating system.

TouchBistro: targeting smaller restaurants.

HarborTouch: Catering to the 1-2 terminal restaurant.

Aldelo: built around an on prem solution.

Positouch

The market is incredibly noisy, but I have reviewed Toast’s win/loss rates against all of the above competitors and Toast consistently wins based on the quality of product and reasonable pricing relative to such a full-suite product.

Looking ahead, catalysts for profitability

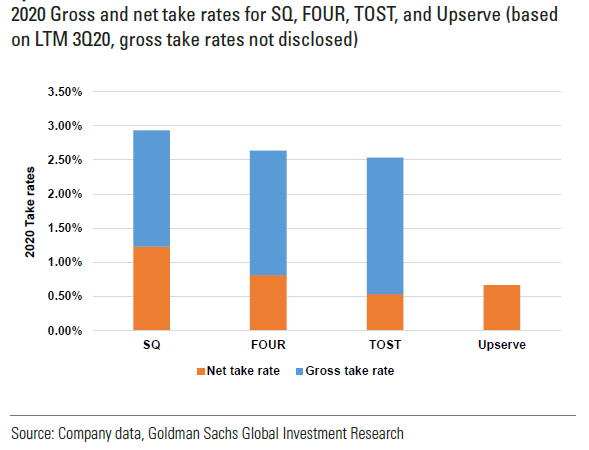

1. ARPU (average revenue per user) increase

I believe that ARPU expansion represents a key growth driver for Toast over time, which should become increasingly important as it gains a larger share of locations.

On the Payments side, I see room for take rates to increase closer to peer levels given where they are at now.

(click to enlarge)

2. Invoice processing and B2B expansion

Toast currently offers several software modules that help streamline operational processes, which saves time/costs for restaurant owners that either manage these processes manually or through point solutions provided by third parties. These offerings currently include integrated payroll processing, labor and inventory management, multi-location menu management, kitchen display systems, and data/analytics.

Toast recently expanded its back office offerings through the acquisition of xtraCHEF, which provides restaurant-specific invoice management software that automates accounts payable workflows and reconciliation of invoices for accounting and vendor payments, while also enabling them to track the P/L of menu items down to the ingredient level and benchmark performance on operational metrics across multiple locations.

While it remains early, as the acquisition only recently closed in June 2021, I believe that B2B represents a meaningful opportunity for Toast to expand its addressable market, by increasing the wallet share obtainable from each live location.

Financials

The revenue number continues to dazzle. For Q3 '21, Toast brought in $468 million of revenues. This was up an eye-catching 105% from the same quarter of 2020. The company's annualized recurring revenue "ARR" also surged 77% year-over-year, indicating that Toast has a stable growth runway ahead of it. So, what's the problem?

Simply put, Toast is generating very little in actual profits from these revenues. The company scored just $83 million of gross profits off its $468 million of revenues. That's just an 18% profit margin. Normally, you'd expect software companies to earn massive gross profit margins. But Toast appears much closer to a low-quality commodity or cyclical business, at least for now.

Here's another way of looking at it. For Q3, Toast had gross payments volume "GPV" of $16.5 billion. Yet, it scored just $486 million of revenues and $83 million of gross profit off those figures. This means that Toast captured 2.9% of its GPV as revenues and just 0.5% of its GPV as gross profit.

The company has more concerning figures as you move down its Q3 earnings press release. For one thing, the company produced negative operating and free cash flow for the quarter. This was actually a worsening from Q3 '20, when the company broke even on a cash flow basis.

Things don't look any better with EBITDA. Even using a favorable adjusted EBITDA basis, the company generated a $10 million EBITDA loss on the quarter versus a breakeven result for the same period in 2020.

Things are set to get even worse in the upcoming holiday quarter; for Q4, the company anticipates losing $40-$50 million of adjusted EBITDA. And, again, you can't just scale out of these sorts of losses since the profit margins here are so anemic.

Key Risks:

Vertical/Geographic concentration: While Toast sees potential to expand

internationally over time, the company currently generates all of its revenue from the US, specifically from the restaurants vertical. As a result, changes that affect the US restaurants industry could be more impactful to Toast relative to peers focused on multiple verticals and geographies.

Competitive pressure: The restaurant industry is highly fragmented, ranging from restaurants with one location that rely on manual processes and legacy POS systems to global enterprises that develop custom-built solutions internally. I believe that Toast is well positioned to gain share from legacy solution providers based on its more comprehensive and modern platform, however, competition among vendors is intense and modern competitors are increasingly investing in vertical-specific solutions. For example, Square, Olo, Clover (owned by Fiserv), Upserve (owned by Lightspeed), Shift4, and Touchbistro each offer modern software-embedded payments solutions specifically built for restaurants. If competitors develop superior products or offer comparable products at more attractive price points, it would negatively impact Toast’s ability to add new locations and retain existing locations, which would create downside risk to forecasts.

Conclusion

I believe Toast represents a compelling investment given it’s expected to grow at around 30% in the next years especially with valuation levels today at 5.8x. I have initiated a small position and look to increase it over the next couple of weeks while closely monitoring the macro situation in the US.

Sources:

CapitalIQ

SEC filings of Toast

Investor relations website

Please note that this article does not constitute investment advice in any form.