Intel Corporation, a turn around story

Company Description

Intel Corporation (NASDAQ: INTC) is a US-based multinational technology company. It designs and manufactures semiconductor chips which are the core technology platforms for computers, IT networks and telecommunication systems. Once considered the sector’s global leader this is arguably no longer the case. If market leadership is reflected in the market capitalization of the company, Intel now rates number three behind Taiwan Semiconductor Manufacturing Company and NVIDIA.

Intel was founded in 1968 by Gordon E Moore (famous for Moore’s Law) and Robert Noyce who are credited with being the co-inventors of the integrated circuit. The company went public with an initial public offering in 1971.

Intel’s principal activities include the design and production of microprocessors, motherboard chipsets, network interface controllers and integrated circuits, flash memory, graphics chips, embedded processors and other devices.

Intel’s key markets include:

Computer market (personal computing and desk-tops).

Server, network and storage platforms (which includes data centres).

Internet of Things – including components for transportation, retail, industrial, infrastructure and home markets.

Computer security and anti-virus software.

Programmable semiconductors (called a field programmable gate array)

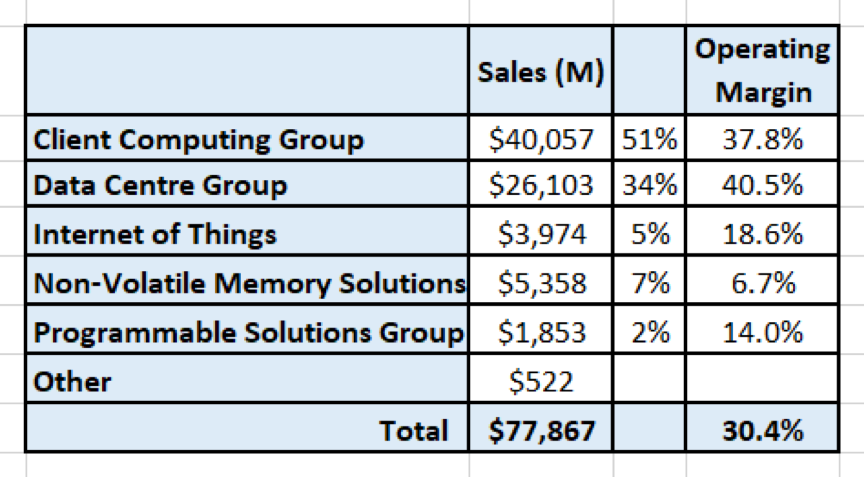

The company currently has 5 reportable operating segments and the 2020 full year sales and margins are shown in the table below:

Source: Data from Intel’s 10-K.

The key difference between Intel and its main competitors is that Intel designs (fabless) and fabricates (foundry) its products in-house. Most other semiconductor suppliers outsource the manufacturing of the actual products to foundries (such as Taiwan Semiconductor Manufacturing Company).

Business Overview

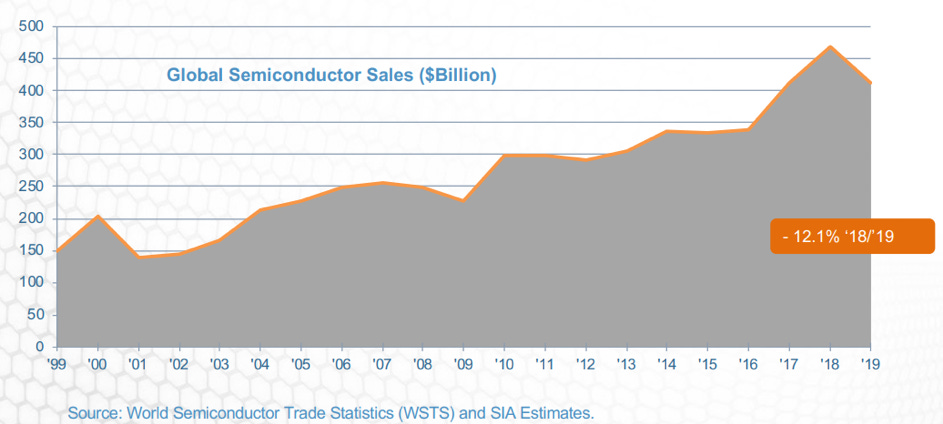

Global demand for semiconductors has been in a long-term secular upswing as shown in the following chart:

The Semiconductor Industry Association (SIA) estimates that the global market had approximate revenues of $US440 B in 2020. Even with the COVID-19 global economic slowdown revenues increased by 7% last year.

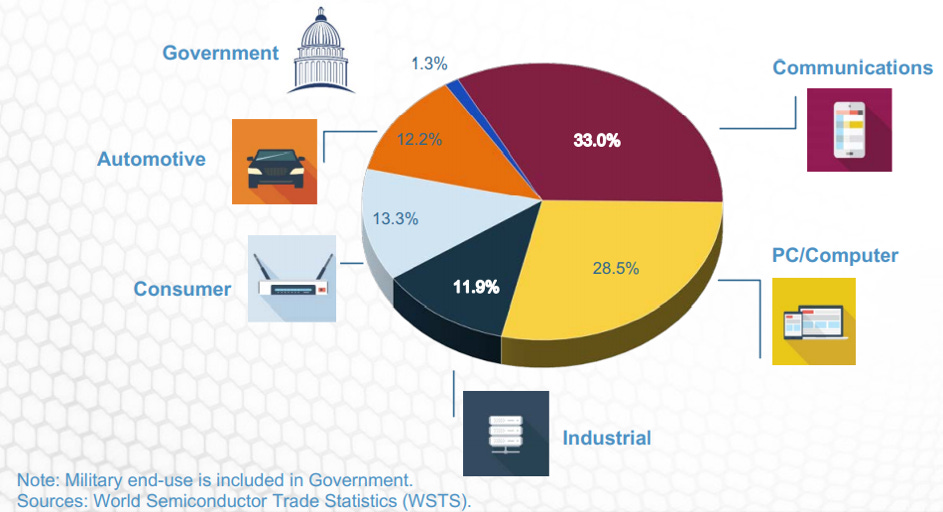

It is perhaps more interesting to segment the market by end-use. SIA estimates the size of the major end use markets in the following chart:

The PC market has surrendered its end-use market leadership to the communications sector. As can be seen from the chart - most of the semiconductor demand is ultimately for consumer products (PCs, mobile phones, etc.) but the mix will change over time as more chipsets are installed into cars and other every-day objects.

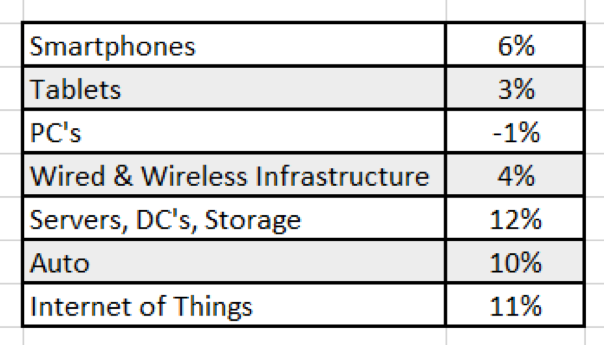

Forecast Segment Growth Rates

Gartner recently forecast that the compound annual revenue growth rate over the next 5 years for the various segments are:

Source: Gartner press release.

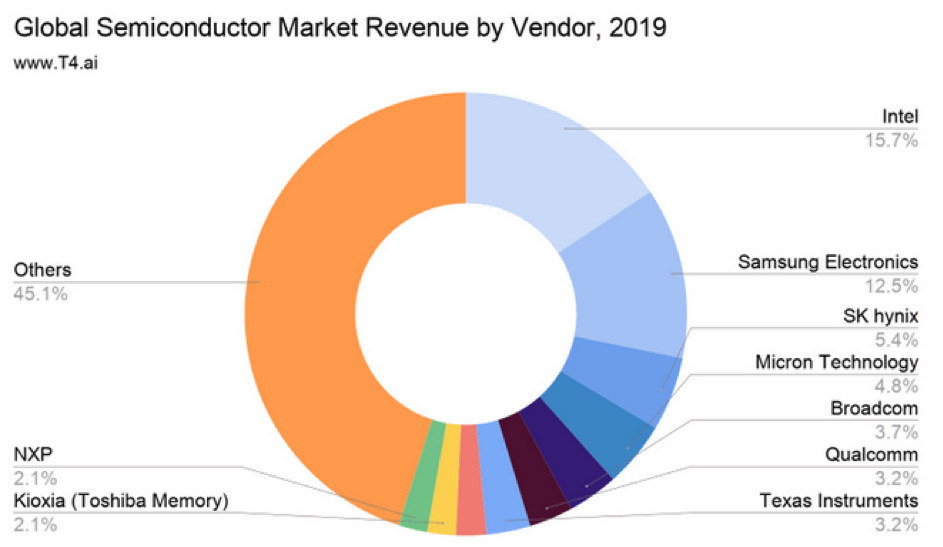

Market Share Split for the Semiconductor Producers

The semiconductor market is very fragmented as shown by the following chart:

Intel is believed to have the largest market share in the sector, but its lead is being progressively eroded over time because Intel does not dominate the faster growing end-use segments.

Foundry Market

Before we start looking at individual companies, I want to cover the Foundry market. It is noted that not all semiconductor suppliers manufacture their own devices. Many companies design their chips but then outsource the manufacture of the device. For example, Nvidia and Qualcomm are major suppliers of semiconductors, but they do not manufacture them.

The Foundry market contains companies who only manufacture devices for third parties and do not produce their own branded products (an example is Taiwan Semiconductor Manufacturing Company) whilst there are others who produce their own branded products as well as manufacturing proprietary devices for third parties (an example is Samsung Electronics).

In August 2020, ReportLinker estimated that the Foundry market was forecast to have revenues of $US141 B by 2027 which equates to a compound annual growth rate of 9.6%.

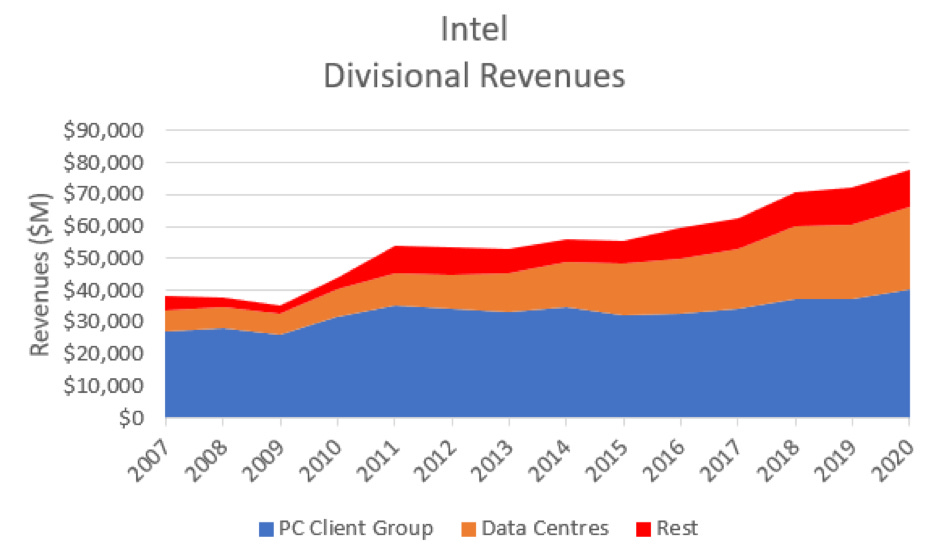

Intel’s Historical Strategy

Intel built its business on the back of semiconductor demand for computers – particularly personal computers (PCs) through the 1990s. This can be seen in the following chart which shows the historical split between Intel’s annual sales for its PC Client Group and its other divisions:

Source: Compilation from Intel 10-K filings.

The PC Client Group’s share of Intel revenues has gone from 71% in 2007 to 51% in 2020 and during this period the PC Client Group revenues have had a compound annual growth rate of 3%.

Although there has been an uptick in PC growth during the COVID-19 crisis, the longer-term trend of limited growth is expected to continue. This means that Intel must innovate and gain more share in its non-traditional markets if it is to grow its revenues and profits.

Intel is in Crisis and Needs to Undertake Major Change

Intel has recently announced a change in leadership and a new CEO took over at the end of February. It has gone from being the technology leader to trailing behind peers as it failed to keep pace with the manufacturing excellence of Taiwan Semiconductor Manufacturing Company and Samsung Electronics. This has resulted in several of Intel’s major customers shifting business to its competitors.

Third Point Investors Limited, an activist investor, wrote an open letter to them in late December 2020. Third Point summarized the issues confronting the board as:

Loss of sector technology and manufacturing leadership.

Loss of human talent to drive innovation.

Third Point believes that the key issue is poor human capital management and that a major strategic review is required to address the current underperformance.

So what is Intel’s current strategy?

Intel identified in 2017 that its priorities were to grow its Data Centre and adjacent market business as well as developing the Internet of Things and devices market.

With the new leadership change, Intel made some key hires and a significant strategic shift.

Intel announced a series of major manufacturing-related announcements that clarified any uncertainties about whether the company intended to keep building its own chips by investing $20 billion to build two new state-of-the-art R&D labs in Arizona focused on chip design.

At the same time, Intel displayed a new willingness to work with other chip foundries on some of the company's own chip designs.

Finally, the company also unveiled plans to open up both its current and planned manufacturing capacity to other chipmakers through the launch of Intel Foundry Services.

So where did Intel go wrong before the leadership change?

The manufacturing division has not been able to deliver up to its historical market-leading standards. This has enabled Intel’s competitors to fill the void which has been created.

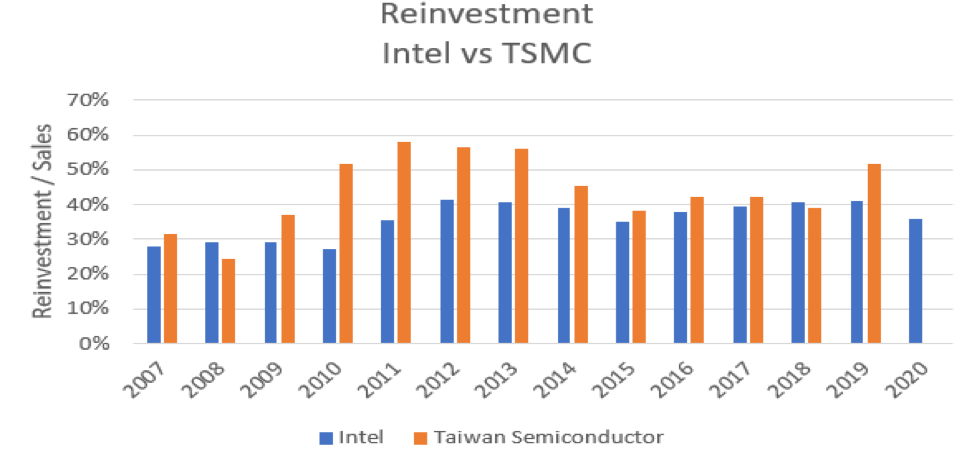

The failure at Intel is a combination of failing to attract and retain high performing staff and a failure to maintain sufficient investment in their technology leadership.

This can be seen from the following chart of historical research and development investment for Intel versus Taiwan Semiconductor Manufacturing Company:

Source: Compilation using companies’ financial filings.

The data shows that TSMC is reinvesting a much higher proportion of its revenues back into its business compared to Intel. It is also noted that Intel’s recent rate of reinvestment has been declining whilst TSMC has been increasing.

Whilst Intel has failed to capitalize on its horizon one strategy it has begun to bulk up its capability in the other adjacent markets such as the Internet of Things.

Intel has also recently announced its intention to sell its NAND flash memory business. The business will be divested in two stages and is ultimately expected to realize $9,000 M. The NAND business currently generates around $5,000 M in revenues but contributes little in terms of operating profit. These funds can be used to reinvest back into Intel’s manufacturing capability.

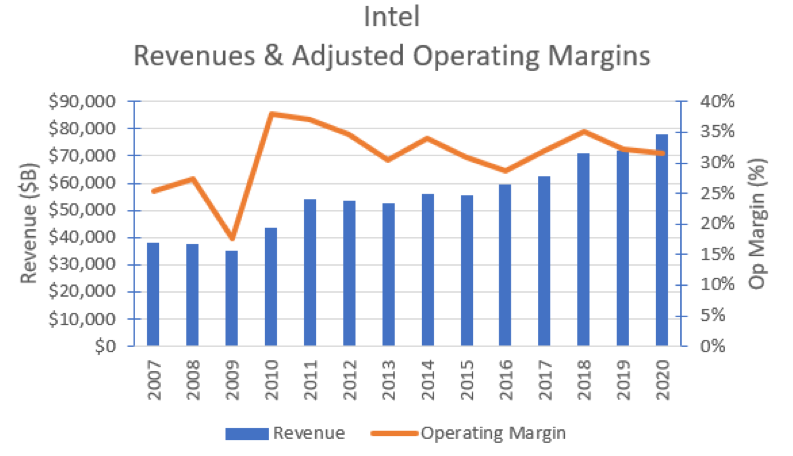

Intel’s Historical Financial Performance

Intel’s historical revenues and adjusted operating margins are shown in the chart below:

Source: Compilation from Intel’s 10-K filings.

The chart indicates that Intel has been growing its revenues over the last 5 years at a compound rate of 7%. At the same time, Intel’s operating margins have been reasonably consistent at around 32%.

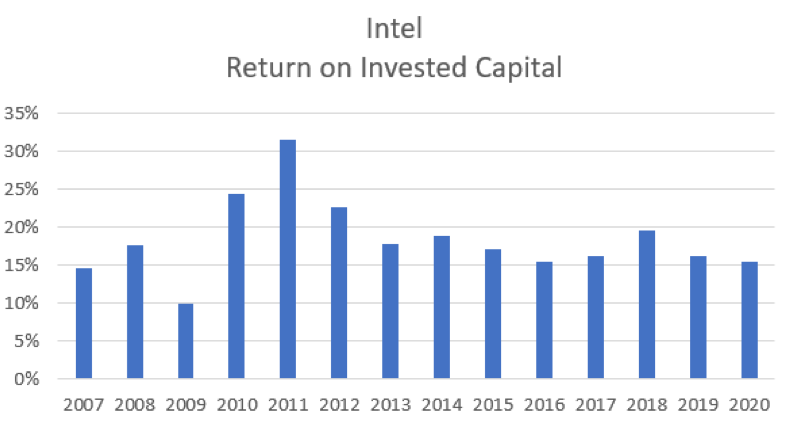

Intel’s Moat

Over the last couple of years Intel’s moat has lost a significant amount of its strength because of its decline in technology leadership. I suspect that the vertical integration between design and manufacturing has led to historical cost advantages, but this advantage may be narrowed into the future as Intel is forced to increase its investment to win back its technology leadership.

The strength of Intel’s moat would normally be measured by its return on invested capital which is shown in the chart below:

Source: Author’s compilation from Intel’s 10-K filings.

Although Intel’s adjusted return on invested capital is not spectacular it is comfortably above its cost of capital. I believe that Intel’s moat has been narrowing over recent years. Clearly there are competitors who have been able to develop similar or better technological capability as Intel.

Recent Share Price Action

Source: Yahoo Finance

Intel's share price over the last year has been very volatile. This is a reflection of both the impact of COVID-19 on the overall market but also on the frustration that investors have had with the performance of the company and the announcement that there would be further delays to the production of 7 nanometer chips. This appears to have marked the recent bottom in the share price and there has been a gradual improving trend ever since.

Intel's capital structure looks sound

I do not have any significant concerns over Intel’s capital structure. The following chart shows the shift in the mix of its debt over time:

Source: Compilation using data from Intel’s 10-K filings.

The debt ratio is relatively high for the sector but is easily serviced by Intel’s reliable cash-flows.

Key Risks Facing Intel

There are several significant risks facing Intel:

Intel’s manufacturing capability has now fallen behind its foundry competitors.

There is a significant risk tied to China trade war as approximately 26% of Intel’s revenues come from the Chinese market

Even if Intel is successful in fixing its capability problems this may still result in declining operating margins as the level of competition intensifies.

The Sector is cyclical and short-term demand is prone to being impacted by global economic conditions.

Conclusion

Intel is a very solid global technology company. It was once considered the market leader, but the company has lost its way over the last few years. The company is undergoing a significant change in leadership and there is a major opportunity for the new leadership to restore the fortunes of this company by recruiting new talented technologists and spending more cash on process technology.

Intel’s future success is strategically important to the United States and as a result management will have the support of the US government. This will possibly be influential in shaping the success of the strategy.

I believe that Intel is a BUY at today’s prices ($51.3 on March 3rd 2021). There should be reasonable confidence that over the long term it should prove to be a good investment given its strategic position for the US economy as a whole. It will however be a tough hold in the short and medium term.