Short Report: Ebang International Holding (EBON)

Short Report: Ebang International Holding (EBON)

Investment Thesis: Short Ebang International Holdings

• Company faces serious operational headwinds in miner production space due to technology obsolescence

• Strategic shift to cryptocurrency exchange space will prove unprofitable

• Customer concentration a great risk to business operations

I. Company Overview:

1) Description:

Ebang International Holdings (Ebang) is a Chinese listed blockchain and telecommunications equipment company company that focuses on designing application-specific integrated circuits, mainly for use in Bitcoin mining machines.

The company is also planning to diversify its offerings to the upstream and downstream blockchain and cryptocurrency industry value chain. On Dec. 31, 2020, it announced that it had completed the initial testing of its cryptocurrency exchange and commenced its public testing. The exchange is scheduled to be launched in Q2 2021.

The company has operations in the Mainland China, the United States, Hong Kong and other countries.

The company was founded in 2010 and is headquartered in Hangzhou, China.

2) Management:

Chief Executive Officer: Dong Hu has been CEO since starting Ebang in 2010. He also serves as chairman of the board of directors. From August 2009, he worked as a teacher of the College of Computer Science and Technology at Zhejiang University of Technology until October 2017. Dong Hu graduated from Zhejiang University of Technology with an undergraduate degree in industrial automation in July 1998. Mr. Hu obtained a Master of Business Administration (MBA) degree from Zhejiang University in September 2008.

Chief Financial Officer: Lei Chen has been Chief Financial Officer at Ebang since April 24, 2020. He served as the Chief Financial Officer of Hailiang Education Group Inc. since January 2014 until September 30, 2016. Prior to that, he worked as an auditing Manager at KPMG and PwC. Mr. Chen received his bachelor’s degrees in International Business and Accounting from Guangdong University of Foreign Studies in 1999. He is a Member of the Chinese Institute of Certified Public Accountants since December 2009.

3) Key Shareholders:

It is worth noting that Dong Hu has 86.5% of the total voting power.

4) Segments:

The company segments its business geographically and by type of product as follows:

5) Financials:

a) Emerging Growth Company Status:

As a company with less than US$1.07 billion in revenue during the last fiscal year, Ebang qualifies as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012. As long as the company remains an emerging growth company, it benefits from exemptions that include being permitted to provide only two years of selected financial data rather than five years.

Thus, the full year financial data available covers 2018 and 2019 only.

b) Financials:

The company’s revenue have been declining steadily since its IPO in 2018 declining by 65% between 2018 and 2019 while bitcoin appreciated by c.108% relative to the USD in the same period.

The company’s revenue declined by c.50% between H1 2019 and H1 2020 at a time where Bitcoin’s value grew by c.21% relative to the USD.

It makes sense to compare the company’s revenue growth to bitcoin’s value growth as the mining equipment the company is making has a value that is directly impacted by the value of bitcoin.

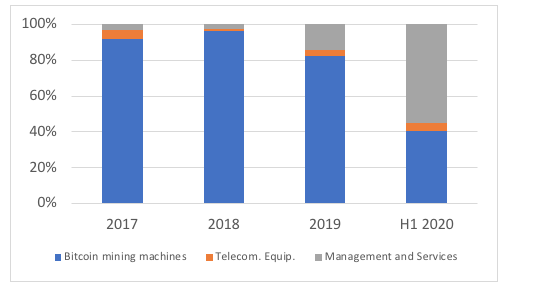

c) Product mix change:

This chart clearly outlines that the firm is switching its strategy focus from bitcoin mining equipment to Management and services while also branding itself as a cryptocurrency company and enjoying high multiples due to this association and expectation of high growth in the future.

II. Industry Overview:

1) Market and Main Competitors:

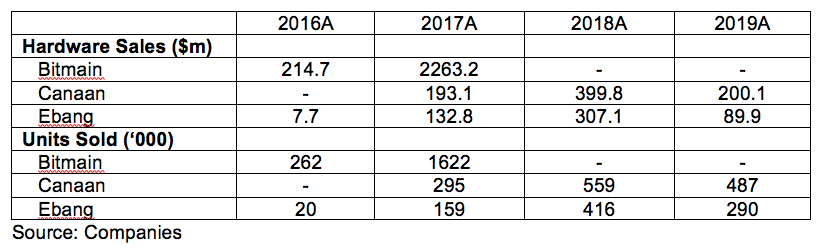

Ebang competes with a couple of other bitcoin mining hardware companies. The most notable ones which have the lion share of the market are Bitmain and MicroBT along with Canaan which IPOed in 2019.

Except Canaan, all of these companies are private but I was able to gather information from Bitmain’s aborted Hong Kong IPO from 2018, Canaan’s 10-K and Ebang’s latest equity offering prospectus from April 2021.

2) Sales Comparison:

Historically, Bitmain has been the dominant player in the space with 17x the revenue and 10x the units sold compared to Ebang in 2017.

III. What the market is getting wrong about Ebang:

While some bullish investors might think that Ebang is ideally positioned to benefit from the increased adoption of bitcoin and thus its price appreciation, I believe that operational, financial and legal headwinds make Ebang a great short play.

1) Customer diversity:

Ebang has a very concentrated customer base all of whom are located in China.

Revenue generated from the top 10 customer represented 57%, 56% and 93% of total sales in 2018, 2019 and H1 2020 respectively.

In H1 2020, the top three customers represented 57% of total sales.

Of the companies’ $109m sales in 2019, only 1.3% ($1.4m) came from the US.

2) Accounts receivables importance and evolution:

Ebang typically requires customer to prepay for its mining equipment before delivery. The accounts receivables of the company have been declining since the IPO and translates low customer stickiness as the miners’ technology becomes obsolete.

So while Bitcoin has been appreciating for the last 2 years, Ebang hasn’t been able to increase orders for their mining equipment.

3) Obsolescence and R&D:

Ebang’s revenue declined 66% to $109m due to a significant drop in bitcoin miner sales.

Even if the company attributed this to the suppressed bitcoin price that year, it is important to note that the industry is extremely competitive and players invest heavily into R&D.

Efficient, more powerful miner are being designed every year and their efficiency is increasing at a pace that Ebang cannot sustain.

In that sense, the company is behind the curve with its last model the Ebit 12 being less efficient than the last two generations of Bitmain and MicroBT.

Efficiency is the most important metric in a miner because they are powered by electricity and a higher efficiency means less costs and higher margins for the customer.

In the meantime, Ebang’s R&D expenses dropped fast between H1 2019 and H1 2020, $7.4m to $3.8m (-48%) and down 80% between 2018 and 2019 ($43.5m and $13.4m respectively). How can you produce more efficient miners when your R&D is dropping?

4) Inventory write-downs:

As new generation miners get released, older ones become less desirable because less efficient and require more energy. Ebang and its competitors end up reducing their prices to incentivize customers.

Despite the price decrease, Ebang has an increasing number of miners that end up not being sold which increases the DSO (days sales inventory) from 142 days in 2017 to 268 days in H1 2020.

Units Sold in thousands:

5) Legal disputes with customers:

Ebang has ongoing disputes with a couple of its largest customers alleging the company not deliver all the products agreed on with the customer refusing to pay the full amount.

6) Future Projects:

Given its lagging miner design, Ebang is now trying to stir away from the hardware to the services sector within the cryptocurrency space and has launched a crypto exchange in April 2021.

This bet, I believe, will prove very unprofitable for the company as there are around 300 exchanges worldwide already in the space with only the top 5 currently profitable.

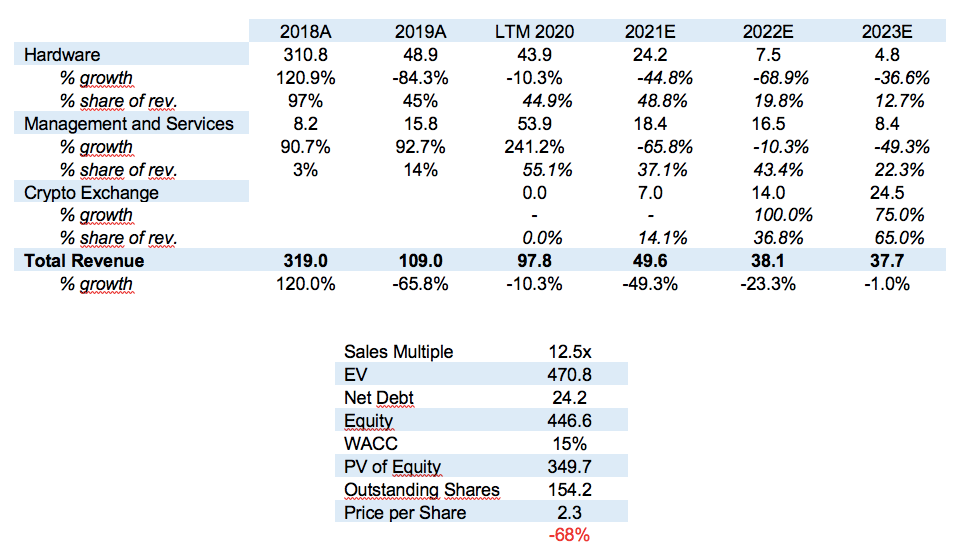

III. Valuation

The top three cyptocurrency exchanges in the world (Coinbase, Kraken, Binance) have an average Sales multiple of 12.5x.

I believe Ebang share price is going to $2.3 (a 68% decrease from current price level) in the next two to three years given the operational, financial and legal headwinds facing the company and because its shift to the cryptocurrency exchange space will reveal an unprofitable strategy in the medium and long term.

References:

https://www.bqintel.com/post/crypto-exchanges-ebitda-multiple